Five Problems. Five Moves.

What the market hasn't fixed and what you should do about it.

There is a category buyer at a major FMCG company in ANZ who knows exactly what their retail media allocation is: the cost of keeping a product on the shelf, expressed in a media budget because “media budget” is a more defensible line item than “supplier levy.” They cannot say this in the meeting where the promotional plan is being discussed. They cannot say it in the annual planning review. They cannot say it at all, because the person across the table controls both the media conversation and the stocking decision, and the brand knows it.

That buyer is not unusual. They are the norm. Part One mapped the market that keeps them there: the duopoly, the challengers, and the payments layer. This edition names the five structural reasons the market is built to obscure performance. Then it shows what to do about it anyway. The central argument is this: the payments networks arriving in ANZ are not additional ad products competing for the media budget. They are independent measurement infrastructure. And they are about to audit everything the grocery networks have been reporting.

I know this from the inside. I led the launch of The Wallet Advantage at Afterpay Ads in November 2025, making it the first payments-native commerce media product formally positioned in the ANZ market. The project ended before it reached full commercial scale. That experience informs the argument in this edition.

Five reasons the market is built this way

The gap between what gets reported and what is true is not an accident

The gap between reported ROAS and incremental ROAS is concrete. A mid-tier FMCG brand running a standard sponsored-product campaign across a major ANZ grocery network will typically see ROAS reported at 3 to 4x. A geo holdout on a comparable campaign, using Circana scan data as the measurement currency, routinely returns 1.4 to 1.8x incrementally. That gap is not a measurement error. It is the intended output of a system optimised to report its best number. Five structural problems make that system work the way it does.

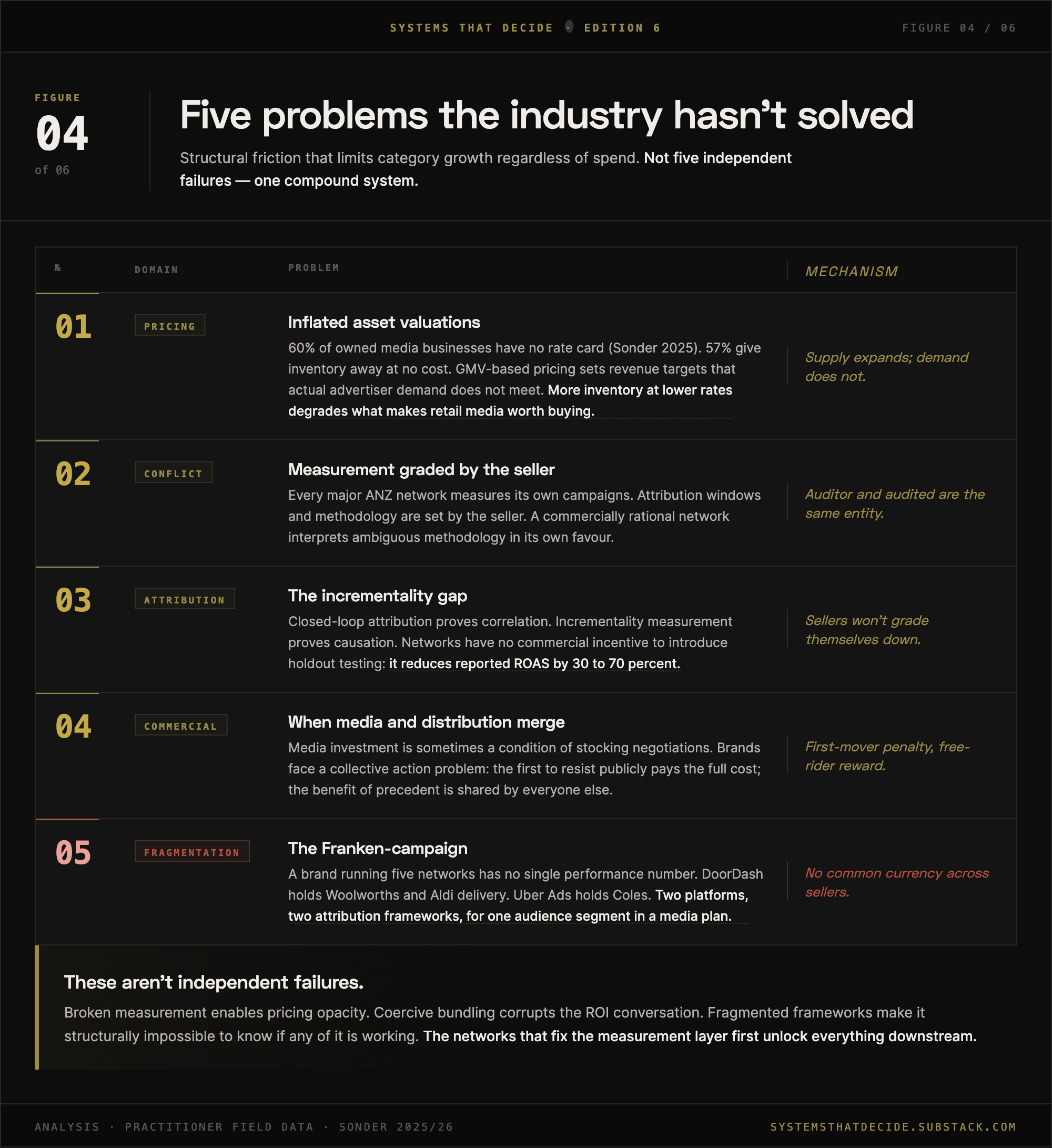

1. Pricing without a benchmark

The most common retail media valuation methodology, a fixed percentage of GMV, is, in Sonder’s words, “a blunt instrument that has wreaked untold havoc for retail media teams.” Networks built on GMV benchmarks set revenue expectations that actual advertiser demand does not meet. The typical response is more inventory at lower rates, which degrades what makes retail media worth buying in the first place.

Sonder’s 2025 Global Market Report finds that 60 percent of owned media businesses globally have no rate card. Buyers negotiate blind against a number that does not exist. Separately, 57 percent are giving owned media to partners at no cost, surrendering $48 million in media value per Retail Aggregator business per year. Not earning it. Giving it away. Less than 30 percent of the $573 billion global owned media opportunity is currently being captured. Over-valuation and under-valuation are both symptoms of the same root cause: there is no independent pricing benchmark. The number the network quotes you is not anchored to anything you can check.

2. Measurement graded by the seller

Every major retail media network in ANZ measures its own campaigns. The attribution methodology is defined by the network. The reporting is produced by the network. The result is delivered to the brand by the network. The conflict of interest is structural, not incidental.

A network interpreting an ambiguous methodology choice, whether to use a 7-day or 14-day attribution window, whether to count view-throughs alongside clicks, has a commercially rational incentive to favour the interpretation that produces a higher ROAS. That is not corruption. It is incentive structure. The ACCC documented the downstream consequences: brands unable to independently verify attribution claims, investment decisions made on ROAS figures with no external validation. The Coles 360 and Circana partnership is the strongest response any ANZ network has made toward accountability. It is not sufficient and it is not universal.

3. The incrementality gap

Problem 2 is about who controls measurement. This one is about what that control conceals. Closed-loop attribution proves correlation. Incrementality measurement proves causation. The retail media industry has sold the former as the latter for five years. Incrementality testing requires a control group, a comparison of purchase rates between exposed and unexposed customers, and an honest accounting of what would have happened without the campaign. None of these steps are in the standard retail media reporting suite. Operationalising them at scale reduces reported ROAS by an estimated 30 to 70 percent depending on the category and network.

The global market has moved. TransUnion and eMarketer research from July 2025 found 52 percent of brands and agencies globally are now using incrementality testing. Google cut its Conversion Lift minimum threshold from approximately $100,000 to $5,000 in November 2025. The online testing tooling exists and is now accessible at meaningful scale. The harder problem for FMCG and grocery categories is offline: capturing in-store sales requires integrating loyalty or point-of-sale data, a step most ANZ campaigns have not taken. The technical barrier is falling. The integration work is the remaining gap.

There is a second dimension to this problem that the industry has not named clearly. April 2026 research from In-Store Marketplace, based on interviews with brands, agencies, and RMN executives across the US and UK, found that in-store media has suffered from what it calls “digital envy”: the assumption that it must replicate one-to-one, closed-loop digital attribution to be credible. The result is a channel evaluated against a framework it was never built for, while the methodologies that actually work for physical retail — matched-market tests and pre vs. post analyses — are treated as second-rate rather than fit-for-purpose. The same research identified four competing scorecards operating simultaneously across agencies, merchants, RMNs, and brand shopper marketing teams. When those scorecards do not align, measurement gridlock occurs regardless of technical capability. The incrementality gap in ANZ is partly a testing gap. It is also a stakeholder alignment problem.

4. When media and distribution merge

The ACCC inquiry and AFGC submissions describe the environment in institutional language: brands presented with media investment requirements as a component of stocking and promotional negotiations. The plain version is this. It is a cost of distribution rendered in media language. The ROAS reported on a bundled investment is not a media performance number. It is a commercial cost with a denominator attached.

The brands in this position face a collective action problem. The first to resist publicly pays the full cost alone, losing shelf priority, promotional placement, and commercial goodwill, while the benefit of establishing a precedent is shared across every brand in the category. No individual brand’s incentive calculation supports being first. The result is an industry where the measurement question is asked in an environment where the buyer knows the answer may affect stocking decisions that extend far beyond media performance. The ACCC inquiry has created a public record. How networks respond to that record will shape the next phase of commercial negotiations.

5. The franken-campaign

Each of the four preceding problems compounds in the multi-network campaign. The incrementality gap is present in each network separately and invisible in the aggregate. Self-reported attribution from five networks with five different methodology frameworks produces five clean numbers that add up to nothing coherent. Budget coercion at the individual network level means the media plan may never have been built on genuine ROI. Inflated valuations stacked across networks inflate the total investment against performance that nobody is measuring in a common currency. The Franken-campaign is not a fifth, separate problem. It is what the first four look like when they are running simultaneously.

A brand running across Cartology, Coles 360, CommBank Connect, DoorDash, and Amazon Ads has no single number that describes overall performance. Audience overlap is unmeasured. Incremental reach from each additional network is unknown. Reaching the full grocery delivery audience in ANZ requires buying both DoorDash Ads (Woolworths and Aldi shoppers) and Uber Ads (Coles shoppers), two incompatible measurement frameworks for what looks like one audience segment in a media plan. Every new launch, Myer with 5.1 million Myer One members, Virgin Australia on Velocity data, adds another incompatible framework to an already incoherent landscape.

Amazon Ads is the exception worth noting. It is the only retail media network in that list that ships measurement infrastructure as standard. Amazon Marketing Cloud gives advertisers the tooling to interrogate fragmentation, run custom audience analysis, and conduct incrementality measurement within Amazon’s signal environment. The fragmentation problem is still real. But Amazon’s approach to it is structurally different from the grocery networks that produce a single clean ROAS number and stop there.

The Franken-campaign will not be solved by the networks. It will be solved, if it is solved, by the independent infrastructure layer: whole-wallet attribution from payments networks, Circana validation extended across the market, or a regulatory reporting standard above a revenue threshold.

What to do with what you now know

Five moves for buying in a market built against you

The data assets are real. The audience advantages are structural. None of that is in dispute. What is in dispute is whether the measurement honestly reflects them. A structural advantage and a system that accurately accounts for it are not the same thing. They have been treated as the same thing for five years. That is the problem. Here is what to do about it.

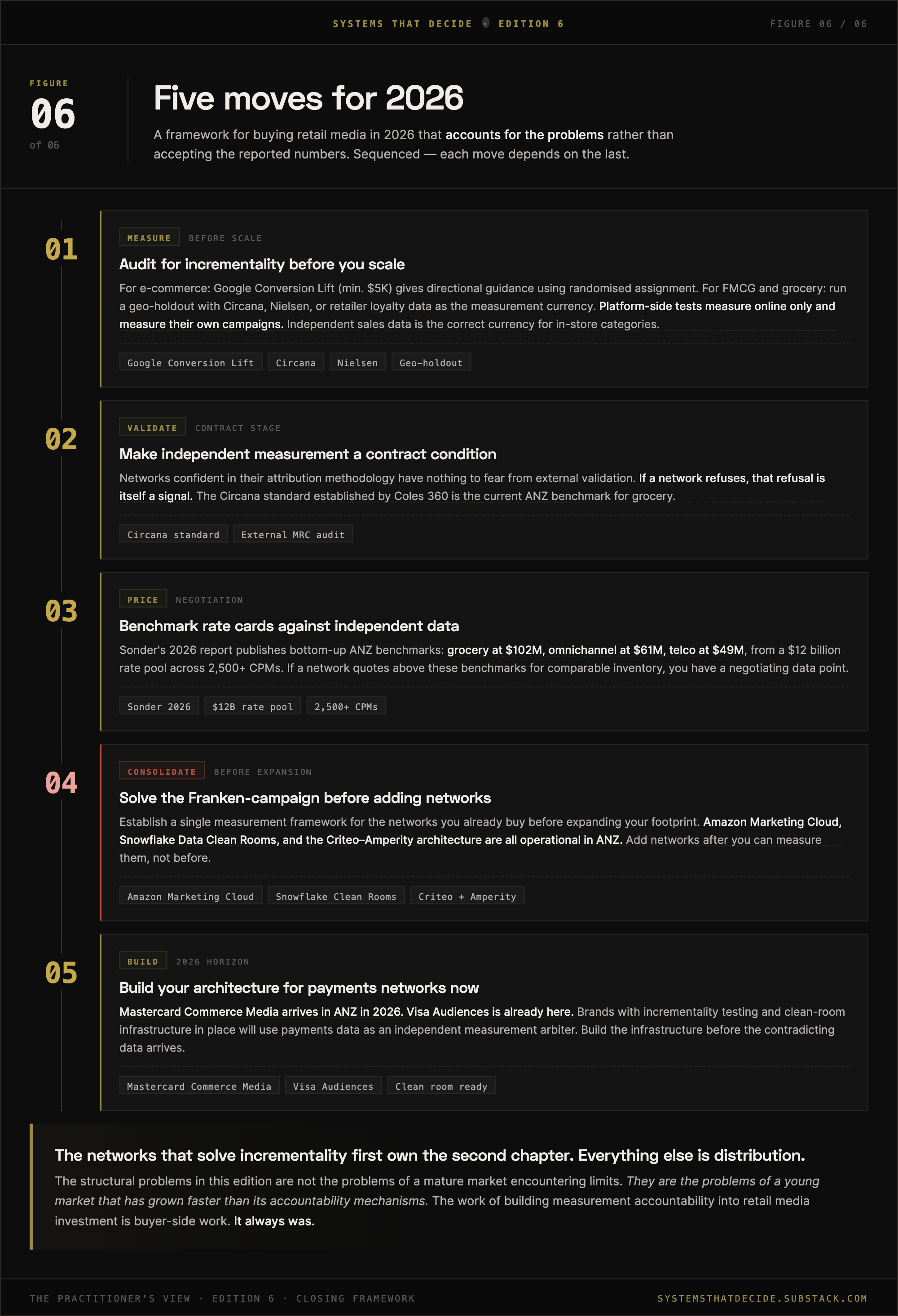

1. Audit for incrementality before you scale

The right test design depends on your category. For FMCG and grocery, where most purchases happen in-store, run a geo holdout with independent sales data as the measurement currency. Select matched geographic markets, suppress the campaign in the control group, and use Circana or Nielsen scan data, or retailer loyalty card data, to compare actual purchase rates. This approach captures offline sales by design and produces a number that reflects what happened at the register, not what was visible in a digital attribution window. Meta’s GeoLift tool is open source and built specifically for this design. For e-commerce and digitally-purchased products, Google Conversion Lift, minimum now $5,000, gives a methodologically sound starting point using randomised user assignment rather than last-touch attribution. Note the structural limit here: Google is measuring the effectiveness of Google campaigns. The conflict-of-interest problem does not disappear just because the methodology is sounder than last-touch. Independent sales data is the correct measurement currency for in-store categories. For those, the geo holdout is the standard, not a supplement.

The test will tell you three things: whether your ROAS holds up incrementally, whether you’re paying for customers who were going to buy anyway, and whether you’re cannibalising organic purchase while paying for attribution credit. None of those answers are comfortable. All of them are more useful than continuing without knowing.

2. Demand independent measurement as a contract condition

Networks confident in their attribution methodology have nothing to fear from independent validation. Make external measurement a procurement condition, not an optional upgrade. If a network refuses, that refusal is itself a signal. The Circana standard established by Coles 360 is the current ANZ benchmark for grocery. Price the risk of self-reported attribution into your investment decision accordingly.

3. Benchmark your rate cards against independent data

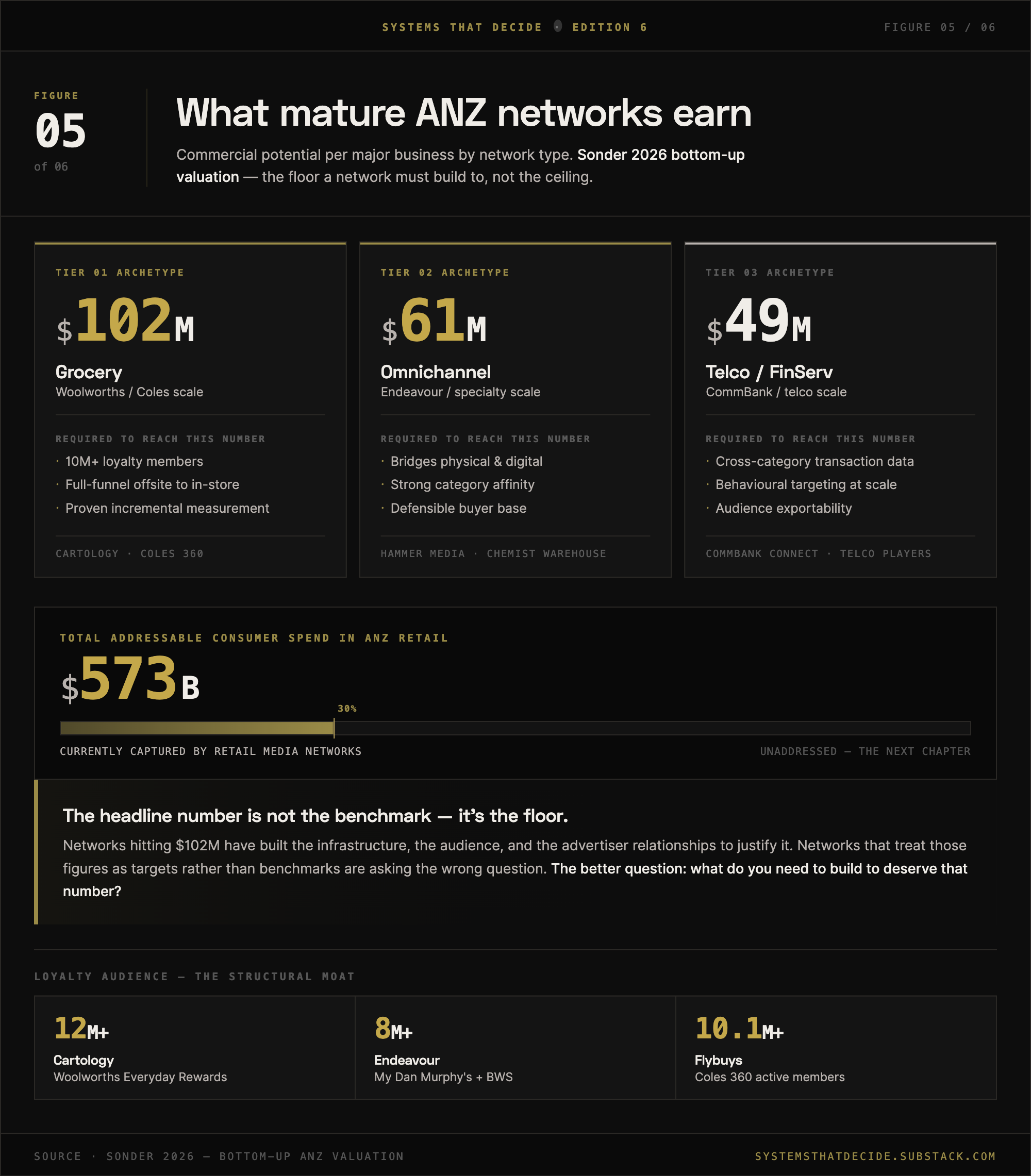

Sonder’s 2026 report publishes the first credible bottom-up commercial potential benchmarks for ANZ by network type: major grocery networks at $102M, omnichannel at $61M, telco at $49M. These are not revenue figures. They are bottom-up estimates of what each network type is capable of earning if its owned media is properly valued and activated, derived from a $12 billion rate pool across 2,500+ CPMs. I should note that Sonder’s commercial model involves selling benchmarking and valuation services to retail networks. Their methodology is transparent and the underlying data is independently derived; the commercial interest is relevant context, not a disqualifying conflict. If the network you’re buying quotes materially above these benchmarks for comparable inventory, you have a negotiating data point. If it quotes below, you have a signal about either rate strategy or inventory quality.

4. Solve the Franken-campaign before adding a network

Establish a single measurement framework for the networks you already buy before expanding your footprint.

Amazon Marketing Cloud deserves more than a passing mention here. AMC is the most measurement-mature clean room available to ANZ marketers today. It runs custom SQL across Amazon’s full signal set, supports incrementality analysis as a native capability, and allows advertisers to bring their own first-party data in for matched-audience measurement across both Amazon and non-Amazon exposure. The conflict of interest is still present and worth naming: AMC measures Amazon campaigns with particular precision, and Amazon has a commercial interest in that result. That context belongs in the room. But the tooling is built to a standard that the ANZ grocery networks have not matched, and brands running Amazon Ads without AMC are paying for measurement capability they are not using. The constraint is not access. It is the data engineering investment required to connect it. Build that capability before you need it to resolve a disputed ROAS number, not after.

Snowflake Data Clean Rooms and the Criteo-Amperity architecture are also operational in ANZ for brands managing cross-network measurement outside Amazon’s environment. Every new network you add without solving the measurement fragmentation deepens the incoherence. Add networks after you can measure them, not before.

5. Build your measurement architecture for the payments networks now

The Wallet Advantage at Afterpay Ads was the first payments-native commerce media product formally positioned in the ANZ market, launching in November 2025. It is no longer operational. Mastercard Commerce Media will follow in 2026. Visa Audiences is already active in ANZ programmatic. The brands that have built incrementality testing and clean-room measurement infrastructure into their buying practice will be positioned to use payments data as an independent measurement arbiter. The brands that have not will be buying on self-reported attribution from networks that a third-party data source now contradicts. Build the infrastructure before the contradicting data arrives, not after.

Three things need to be in place before payments networks can serve as an independent measurement arbiter. First, establish an incrementality baseline now. Visa Audiences is active in ANZ programmatic today and can serve as that baseline source: a number you own, measured against a methodology you control, before Mastercard Commerce Media is fully operational and before a contradicting result arrives in a briefing room. Second, connect clean-room access. Snowflake Data Clean Rooms and the Criteo-Amperity architecture are both live in ANZ. Connect your CRM or loyalty data to one of them before you need to cross-reference a disputed ROAS number, not after. Third, agree internally on what “independent measurement” means before a contradicting number arrives. This sounds procedural. It is not. If procurement, media, finance, ecommerce, and category teams do not agree on what counts as independent evidence, every contradicting result becomes a political argument. The network has one number. The agency has another. The category buyer has a third. Finance does not trust any of them. The brands that define the process first will use payments data as leverage. The brands that do not will dispute the result instead..

The measurement framework we were building at Afterpay Ads tracked incremental lift across GPV, total sales, AOV, share of wallet, LTV, and new vs. returning buyers. That is not a media metric stack. It is a business performance stack. We were close. The project ended before it launched. First-mover advantage in payments commerce media requires institutional backing to compound. The data asset and the positioning exist. The execution capacity does not. The brands that build measurement infrastructure now are entering a relationship with payments networks that are still developing their commercial scale. That is the right moment to establish a baseline and set the terms. The moment that follows it is not.

Retail Media Won The Lower Funnel. The Question Is Whether It Deserved To.

The ANZ retail media market in 2026 is at the end of its first chapter. The category was built on the promise of closed-loop measurement. The second chapter will be built on whether those loops actually closed.

The dominant grocery networks in ANZ hold genuine data assets: longitudinal household purchase history, in-store screens, and supplier relationships built over decades. Those distribution moats are real and durable. The measurement accountability gap is equally real. A distribution moat and an independent account of whether the media worked are not the same thing. The networks that close that gap first will hold the stronger position. The ACCC has applied the regulatory pressure. The payments networks will apply the data pressure. The first major brand to run a geo holdout, publish the result, and reallocate accordingly will apply the social pressure. The sequence is not speculative. It is in motion.

No grocery network is exempt from this dynamic. The payments networks arriving in ANZ are not additional options for a media plan. They are whole-wallet attribution infrastructure that will make every grocery network’s closed-loop claims look like a subset. When Mastercard Commerce Media is fully operational in ANZ, CommBank Connect’s positioning does not gradually evolve. It flips. From an interesting ANZ experiment to a local node in a globally scaled measurement architecture that sees every transaction across the wallet.

The networks that solve incrementality first will own the second chapter. Everything else is distribution.

The structural problems across these two editions are not the problems of a mature market encountering its limits. They are the problems of a young market that has grown faster than its accountability mechanisms. That gap will close through industry discipline or regulatory intervention. By the end of 2026, at least one major ANZ brand will publish the results of a geo holdout against a grocery network campaign. When that happens, the market’s relationship with self-reported attribution will not recover. The brands waiting for the industry to solve this on its own behalf are waiting for an incentive structure that does not exist. The work of building measurement accountability into retail media investment is buyer-side work. It always was. That category buyer who knows the number but cannot say it in the meeting? The payments networks will say it for them.

I spent the last year of my career building the product that was supposed to say it first. The gap between what brands think is working and what is actually working is real. We measured it. The project ended. The gap did not.

If you have run a geo holdout against a retail media campaign in ANZ and have results, I want to hear what you found. Real numbers from real campaigns are the fastest way to move this conversation forward. The more buyers share, the harder it becomes for the market to stay comfortable with self-reported attribution.

Systems That Decide publishes on the infrastructure of decision-making in marketing and advertising. If this edition was useful, share it with someone who is still treating the seller's number as the real number.